Background. The dental education landscape in the U.S. is changing. More programs are opening up across the country, the student body is becoming more diverse in terms of gender and race/ethnicity, and the number of enrollees and graduates is increasing year over year. Dental education is facing a great disruption that may stunt this growth. Starting July 1 of this year, first-year dental students will face new limitations of how much they can borrow in federal loans to pay for dental school. The new cap on student loans passed under the One Big Beautiful Bill Act (OBBBA) will limit borrowing to $50,000 per year for professional degree programs, including dentistry. Average dental student borrowing goes well over the new $50,000 limit in nearly every dental program in the U.S. In fact, dental education represents the largest gap between average annual borrowing and the new cap when compared to medicine and other health care education programs. In short, the new borrowing caps may put dental school out of reach for some students.

___________________________________________________________________________________

Dental education represents the largest gap between average annual borrowing and the new cap when compared to medicine and other health care education programs.

___________________________________________________________________________________

Who will be affected by the new federal borrowing limits? For the 2024-25 academic year, nearly $2 billion ($1.92B) in federal loans was disbursed to over 20,000 dental students. This category of funding represented the vast majority (84.9%) of student financial assistance reported by schools that year, benefiting nearly three-quarters (72.4%) of dental students. The average amount provided in 2024-25 to students who received a federal loan was $95,455, an amount nearly twice that of the new annual loan cap.

Dental students typically pay for their education through federal Graduate PLUS loans, which allow them to borrow the full extent of their tuition and fees, including health insurance and housing. Grad PLUS loans have a fixed interest rate of 8.9% and have no set credit score threshold qualifications. However, the Grad PLUS loan program will be phased out on July 1 as the new professional loan caps go into effect, strictly limiting borrowers to $50,000 per year with no other forms of federal loans available.

What might happen. There are several potential outcomes to the new loan caps and the elimination of the Grad PLUS option that could change the landscape of dental education. The first outcome is that students may look for alternative sources of financing. However, this could be unrealistic unless major shifts happen in private sector lending practices or significant investments are made to expand existing scholarship or tuition credit programs. Unlike federal loans, the interest rates of private dental school loans can range from 3% to 18% and can be varied instead of fixed. Also, unlike federal loans, obtaining private loans depends on the borrower’s credit worthiness; those with credit score ratings of less than 670 or those with no credit history whatsoever are typically denied. An estimated one-quarter of students in professional health programs are disqualified by these conditions. Without regulatory reforms to the private credit loan industry, prospective dental students from disadvantaged backgrounds could be barred from dental school altogether or forced into predatory loans with very high interest rates.

Another potential outcome is that the debt burden among dental graduates could worsen, especially for those who can only secure the cost of their education through increased reliance on private loans. Reliance on private loans may impact graduates’ ability to benefit from federal loan repayment programs available to new dentists who agree to treat underserved populations. For example, the National Health Service Corps (NHSC) offers recent graduates working within health professional shortage areas a $50,000 loan repayment award in exchange for a full-time two-year service commitment. Individual states offer similar incentives through state-loan repayment programs (SLRPs). However, these rewards would only apply to qualifying federal loans and are only helpful to dental students after graduation. These programs will not help prospective students pay for their dental school upfront.

___________________________________________________________________________________

Without regulatory reforms to the private credit loan industry, prospective dental students from disadvantaged backgrounds could be barred from dental school altogether or forced into predatory loans with very high interest rates.

___________________________________________________________________________________

In addition to reforms in private lending, more scholarship opportunities could offset restrictions in borrowing. For example, the U.S. Army’s Health Professions Scholarship Program grants dental students full tuition scholarships and a monthly stipend for each academic year. However, this program and others like it only benefit a small number of students. Policy changes may need to shift loan repayment incentives to apply to entry into dental school rather than exit from dental school.

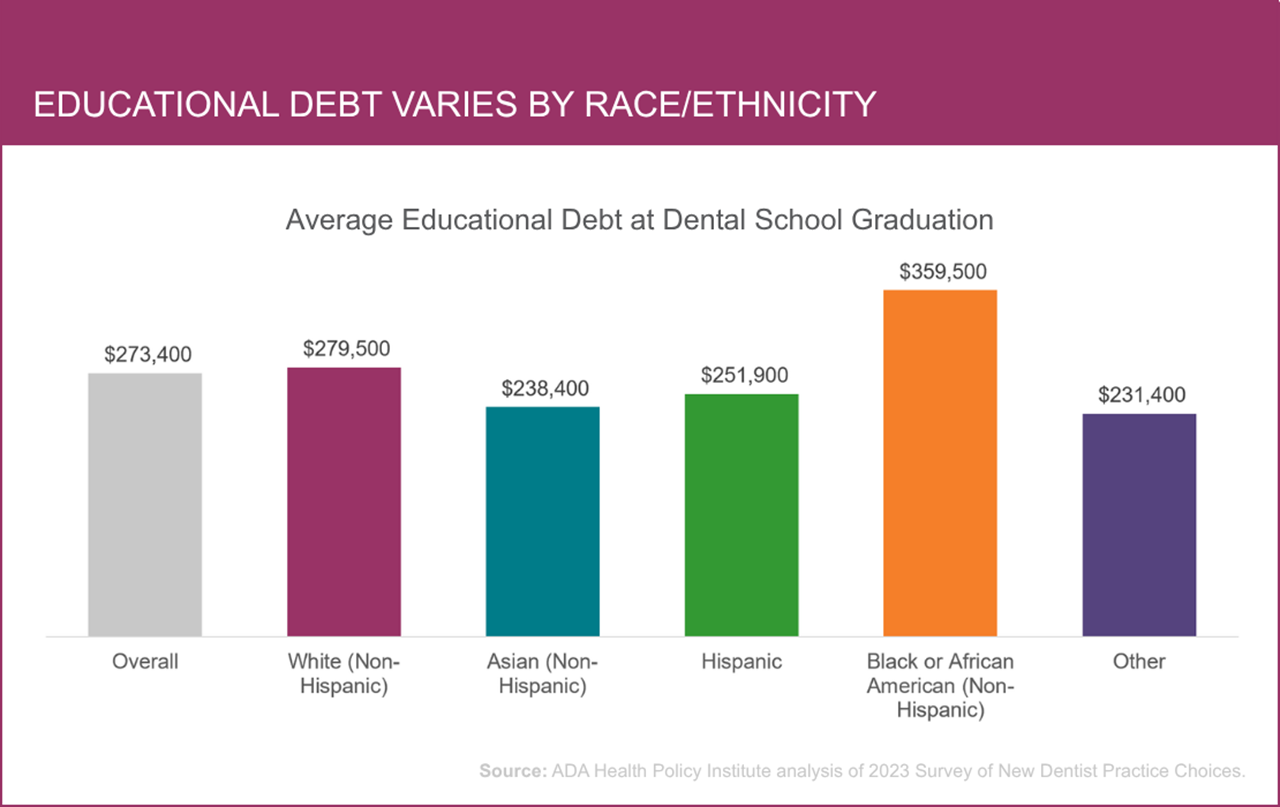

Another potential implication of the new federal loan caps might be that fewer people will apply to dental school. Prospective students, in the face of borrowing constraints, may opt for professions with lower overall education costs such as medicine, veterinary medicine, and optometry. In the case of dentistry, it is important to note that currently there is a 1.8 to 1 ratio of qualified applicants to admitted students across all dental schools in the U.S. Thus, a decrease in applicant numbers might not translate to lower enrollment since there is an excess demand for seats in dental schools. However, the new loan caps may shift the dental student profile in a new direction. For example, there would likely be more affluent students applying to dental school. Currently, 18% of dental students graduate without debt, and the main source of financing for these students is family and friends followed by grants, scholarships and personal savings. The majority of prospective dental students would not have the benefit of scholarships and savings that can cover the full cost of dental school. Federal loan restrictions could also lead to less diversity within the applicant pool. Black dental students, by far, graduate with the highest debt levels and are among the most underrepresented racial groups in the dental profession.